All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Give up periods generally last three to 10 years. Because MYGA prices change daily, RetireGuide and its companions upgrade the adhering to tables below regularly. It's crucial to inspect back for the most current information.

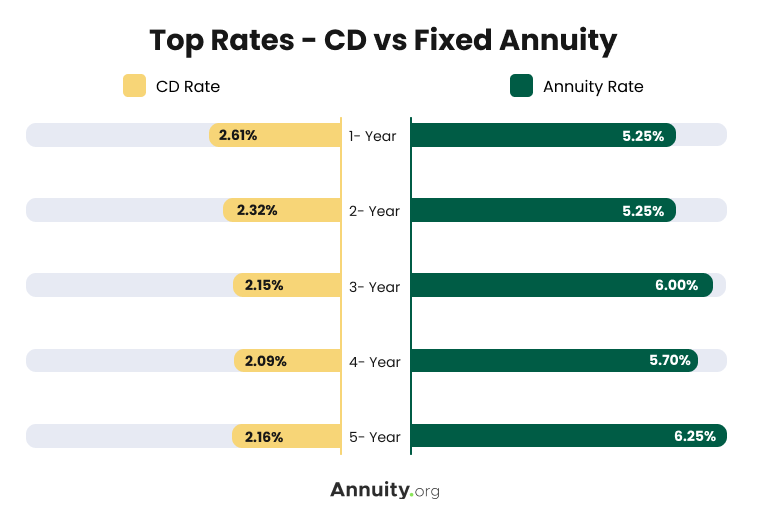

A number of elements determine the price you'll receive on an annuity. Annuity prices have a tendency to be greater when the general degree of all rate of interest is greater. When purchasing fixed annuity prices, you may locate it practical to compare prices to certifications of down payment (CDs), an additional popular option for risk-free, dependable growth.

In general, fixed annuity rates outpace the rates for CDs of a comparable term. Other than earning a greater rate, a fixed annuity might offer better returns than a CD since annuities have the advantage of tax-deferred development. This indicates you won't pay tax obligations on the rate of interest made up until you start obtaining settlements from the annuity, unlike CD rate of interest, which is counted as gross income every year it's earned.

This led numerous professionals to think that the Fed would decrease prices in 2024. However, at a policy discussion forum in April 2024, Federal Get chair Jerome Powell recommended that prices may not come down for time. Powell stated that the Fed isn't certain when passion price cuts could take place, as rising cost of living has yet to fall to the Fed's criteria of 2%.

Best Annuity Leads

Bear in mind that the most effective annuity prices today may be different tomorrow. It is essential to get in touch with insurance provider to validate their certain prices. Begin with a totally free annuity assessment to find out just how annuities can aid money your retirement.: Clicking will take you to our companion Annuity.org. When contrasting annuity rates, it is very important to conduct your very own research and not entirely select an annuity just for its high price.

Take into consideration the kind of annuity. A 4-year fixed annuity might have a greater rate than a 10-year multi-year ensured annuity (MYGA).

The guarantee on an annuity is just comparable to the business that provides it. If the firm you purchase your annuity from goes broke or bust, you could lose money. Check a business's financial stamina by getting in touch with country wide acknowledged objective rating firms, like AM Ideal. A lot of specialists advise just thinking about insurance providers with a rating of A- or above for lasting annuities.

Annuity revenue rises with the age of the buyer because the earnings will be paid in less years, according to the Social Safety And Security Administration. Do not be surprised if your price is higher or less than a person else's, even if it coincides product. Annuity rates are just one factor to consider when acquiring an annuity.

Comprehend the fees you'll have to pay to provide your annuity and if you require to cash it out. Squandering can cost as much as 10% of the worth of your annuity, according to the Wisconsin Office of the Commissioner of Insurance. On the other hand, management charges can accumulate gradually.

Annuities Trusts

Rising cost of living Inflation can consume up your annuity's value gradually. You could take into consideration an inflation-adjusted annuity that improves the payouts in time. Understand, however, that it will considerably lower your preliminary payouts. This implies much less money early in retirement however even more as you age. Take our complimentary quiz & in 3 easy steps.

Check today's lists of the ideal Multi-year Surefire Annuities - MYGAs (updated Thursday, 2025-03-06). For professional help with multi-year ensured annuities call 800-872-6684 or click a 'Get My Quote' switch next to any annuity in these lists.

You'll additionally appreciate tax benefits that checking account and CDs don't offer. Yes. Most of the times postponed annuities allow a total up to be taken out penalty-free. However, the allowed withdrawal quantity can differ from company-to-company, so make certain to review the item brochure thoroughly. Deferred annuities usually allow either penalty-free withdrawals of your made interest, or penalty-free withdrawals of 10% of your agreement value every year.

The earlier in the annuity period, the higher the fine portion, described as abandonment costs. That's one reason that it's ideal to stick to the annuity, as soon as you devote to it. You can pull out whatever to reinvest it, yet before you do, see to it that you'll still prevail by doing this, also after you figure in the abandonment fee.

The abandonment charge can be as high as 10% if you surrender your contract in the first year. A surrender fee would be billed to any kind of withdrawal better than the penalty-free amount permitted by your deferred annuity agreement.

As soon as you do, it's best to persevere throughout. You can establish up "methodical withdrawals" from your annuity. This suggests that the insurer will certainly send you settlements of rate of interest monthly, quarterly or yearly. Utilizing this strategy will not touch right into your original principal. Your other option is to "annuitize" your delayed annuity.

North American Company Annuities

This opens a range of payment choices, such as income over a single lifetime, joint lifetime, or for a specified period of years. Many deferred annuities permit you to annuitize your agreement after the very first contract year. A significant distinction remains in the tax obligation treatment of these products. Rate of interest earned on CDs is taxed at the end of annually (unless the CD is held within tax qualified account like an IRA).

The rate of interest is not taxed up until it is eliminated from the annuity. In other words, your annuity expands tax deferred and the interest is intensified every year. Comparison shopping is constantly an excellent idea. It's true that CDs are insured by the FDIC. Nonetheless, MYGAs are guaranteed by the specific states generally, in the variety of $100,000 to $500,000.

Traditional Annuity

Either you take your cash in a lump sum, reinvest it in one more annuity, or you can annuitize your agreement, transforming the swelling amount into a stream of revenue. By annuitizing, you will just pay taxes on the rate of interest you get in each payment.

These functions can vary from company-to-company, so be sure to explore your annuity's death advantage attributes. With a CD, the interest you earn is taxed when you gain it, even though you do not get it up until the CD develops.

So at the very the very least, you pay taxes later on, instead of sooner. Not only that, however the worsening interest will certainly be based upon a quantity that has actually not already been taxed. 2. Your beneficiaries will certainly get the complete account worth as of the date you dieand no surrender charges will be subtracted.

Your beneficiaries can choose either to get the payment in a lump amount, or in a series of revenue settlements. 3. Typically, when somebody dies, also if he left a will, a judge chooses that gets what from the estate as occasionally loved ones will argue regarding what the will certainly ways.

It can be a long, made complex, and very expensive procedure. Individuals go to wonderful sizes to prevent it. With a multi-year fixed annuity, the proprietor has actually plainly marked a beneficiary, so no probate is required. The cash goes directly to the beneficiary, no doubt asked. If you add to an individual retirement account or a 401(k) strategy, you get tax obligation deferral on the incomes, similar to a MYGA.

{kind=link}

Table of Contents

Latest Posts

Annuity Inflation

Security Benefit Annuities

Fixed Annuity Safe

More

Latest Posts

Annuity Inflation

Security Benefit Annuities

Fixed Annuity Safe